The Skift Research team recently published our much anticipated Hotel Distribution Outlook 2024, and one of the key takeaways was that, by 2030, direct digital channels could overtake online travel agencies as the dominant distribution channel for hoteliers.

We said direct channels could potentially generate more than $400 billion of hotel gross bookings versus $333 billion from OTAs.

Our report generated buzz across the industry. Hotels vs. OTAs is – and always will be – a topic of much heated debate. Many are skeptical that the direct channel could overtake booking sites.

But is our forecast really that controversial? The tools that drive direct bookings have improved dramatically over the past decade and big hotel brands have made deep inroads into owning their customers. The trend toward direct booking is clear.

Will the shift happen by 2030 as our initial forecast says? We can’t say for sure – 5 years is a long time, and, as we note, OTAs will continue to be critical. But let’s look more closely at our forecast:

Digging Deeper

Our report was based on a proprietary survey of hoteliers involved in ownership or operations. We asked about what their current distribution mix looks like today, what they predict the mix will look like by 2030, and what their ideal mix would be.

Based on these survey responses, and our estimates for the global hotel gross bookings market size, we came to a dollar value for how much hotel gross bookings would be coming from direct vs indirect distribution channels. These numbers were based on the 2030 hotelier estimates, which call for a 50/50 first- vs. third-party channel split, a reasonable scenario in our view.

We did not base any of our 2030 estimates off of hoteliers’ “ideal” distribution mix, which called for two-thirds of bookings to come from direct channels.

It is no surprise that hoteliers want more direct bookings and it’s worth emphasizing here that we expect indirect distribution – such as from the OTAs – will remain a prominent distribution channel for the foreseeable future.

So, what other analysis gives us confidence that there could be a noticeable shift towards direct?

Firstly the major hotel groups have reported on it. On the third-quarter 2022 earnings call, Leeny Oberg, CFO of Marriott said that “since 2019, our share of room nights booked through direct digital channels has increased more than 5 percentage points to 38% while our distribution through OTAs has risen by less than 1 percentage point to 12%.”

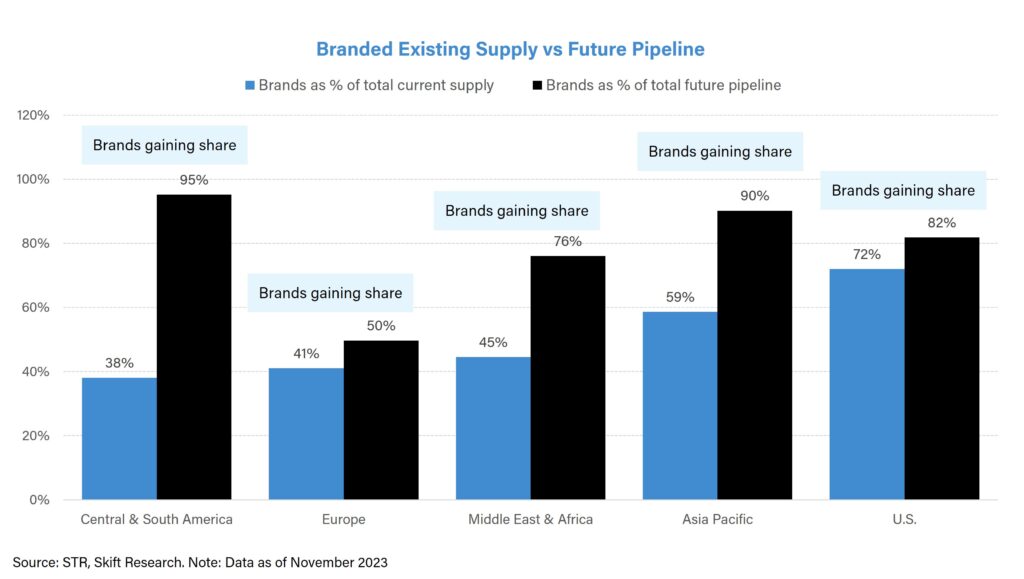

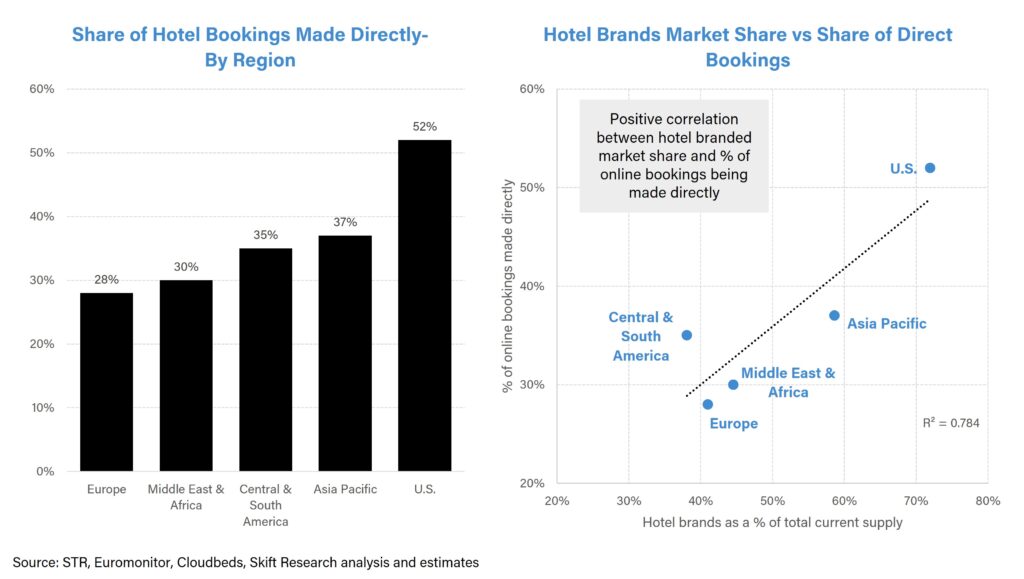

There is also a long-term structural shift towards branded hotels across the world. The chart below shows that hotel brands are expected to gain share from independent hotels in every region of the world…

…and with there being a strong correlation between branded market share and share of bookings made directly, as shown in the scatter chart below, we should expect direct booking share to rise over time.

But what about the independent hotels who don’t want to join a branded network?

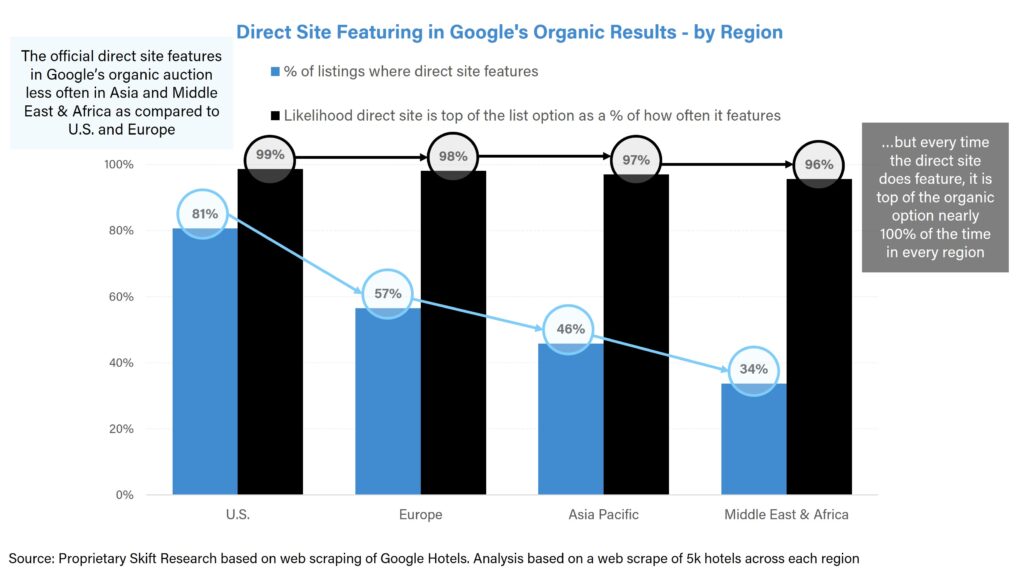

For starters, under pressure from regulators, Google is making it easier and cheaper for independents to compete in metasearch. Google’s introduction of organic search results in 2021 has played a key role in democratizing the distribution landscape, reducing the dominance of the Expedia-Booking duopoly and giving more power to direct hotel sites.

Our recent report analyzing Google Hotels data revealed that Google’s organic search consistently prioritizes direct hotel sites over OTAs across all regions, with direct sites often appearing at the top of search results.

There are many other factors coming together to help independents drive direct bookings today. Social media is leveling the playing field in terms of direct outreach.

Revenue and channel managers are building SaaS tools that have low upfront install costs. This helps make it easier for budget-constrained hotels to install modern direct booking tools by converting big upfront CapEx spends into more affordable monthly OpEx.

Finally, the growth of soft-brands, mini-brands, partnerships, and rewards platforms all make it easier for independents to tap into the benefit of loyalty and repeat customers.

The debate between OTAs and direct bookings is a central theme in Skift’s research. Fundamentally, the ideal distribution strategy is not straightforward, especially in an increasingly fragmented market where traveler preferences, supplier responses, and new distribution models are disrupting the norm.

Importantly, in the face of new competition from external platers, neither direct hotels nor the OTAs are going to relent market share without a fight. Direct hotels are investing heavily into loyalty and personalized experiential offerings, whilst the OTAs are pushing back with new initiatives such as expansions into new verticals, investment into increased efficiencies, and ways to bypass Google through B2B and social media marketing.

Bottom line: the next decade will be driven by innovation and new ventures. We at Skift will continue watching closely.